ChatGPT

ChatGPT

Claude

Claude

Grok

Grok

Perplexity

Perplexity

Gemini

Gemini

Why virtual cards fit ad spend

Ad platforms work on a spend-now, bill-later model. They run your campaigns, then pull whatever they spent from the card on file. The platform's daily budget is a guideline, not a guarantee, and a bid change, a viral post, or a billing glitch can blow past it before you notice. A virtual card adds a real ceiling the platform cannot cross, because the card itself will not carry a charge above the limit you set.

Three things stop happening the day you switch:

- One shared card funding everything. A single company card stops sitting on every ad account, where one problem can drain all of them.

- Overspend reaching your main account. A runaway campaign or billing spike hits that card's limit, not the card you use for payroll and rent.

- One decline taking down every campaign. When each account has its own card, a single declined card cannot pause your entire advertising program.

The right question isn't “do I trust the platform's budget cap?” It's “what is the most I am willing to spend on this account this month, and how do I make that a hard number?” A virtual card is how you make it hard.

What a virtual card actually is

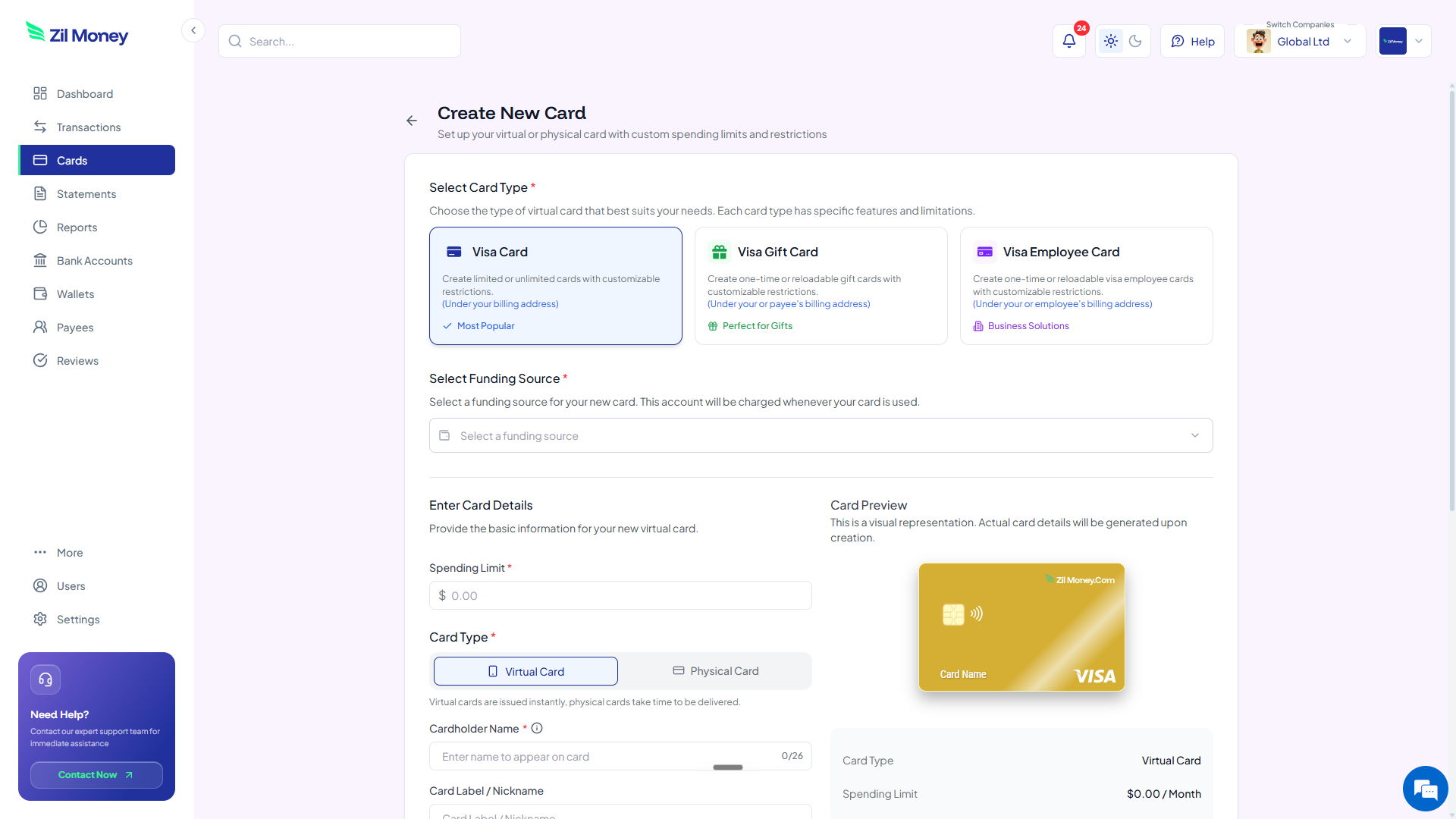

A virtual card is a real Visa card that lives on your screen. It has a 16-digit number, an expiration date, and a CVV, just like the card in your wallet. The difference: you create it when you need it, set its spending limit, and adjust or cancel it whenever you want. You can run one card per ad account, all from the same dashboard.

It works wherever Visa is accepted, including ad platform billing, online checkouts, and in-app purchases, plus Apple Wallet or Google Wallet where supported. A platform's billing page treats it like any other Visa, so nothing about your setup changes except where the ceiling lives.

For a quick visual of how a card is built, the homepage shows the dashboard flow. If you are splitting budgets across teams as well as channels, the guide to giving every department its own budget pairs well with this one.

A virtual card is a Visa you create per ad account. Set the limit to that account's monthly budget, restrict it to the ad platform where supported, and raise, lower, or cancel it as campaigns change.

How to control ad spend with a virtual card in four steps

Here's the full workflow. Read it once and you can run it for every account. Setting up the first card is straightforward, and every card after that is faster.

-

Set the budget as the limit.

Decide the most you want a given ad account to spend this month. That number becomes the card's spending limit, so the platform can spend up to your budget and charges above it can be blocked based on your card controls.

-

Create one card per ad account.

In Virtual Card Maker, create the card, set the limit, and label it by channel or client, for example “Search, Acme Co.” The card shows up in your dashboard with a fresh 16-digit number, expiration, and CVV.

-

Add the card to the ad account and restrict the merchant.

Enter the card as the billing method inside the ad platform. Where supported, restrict the card to that platform, so the number cannot be charged anywhere else if it is exposed.

-

Watch and adjust from your dashboard.

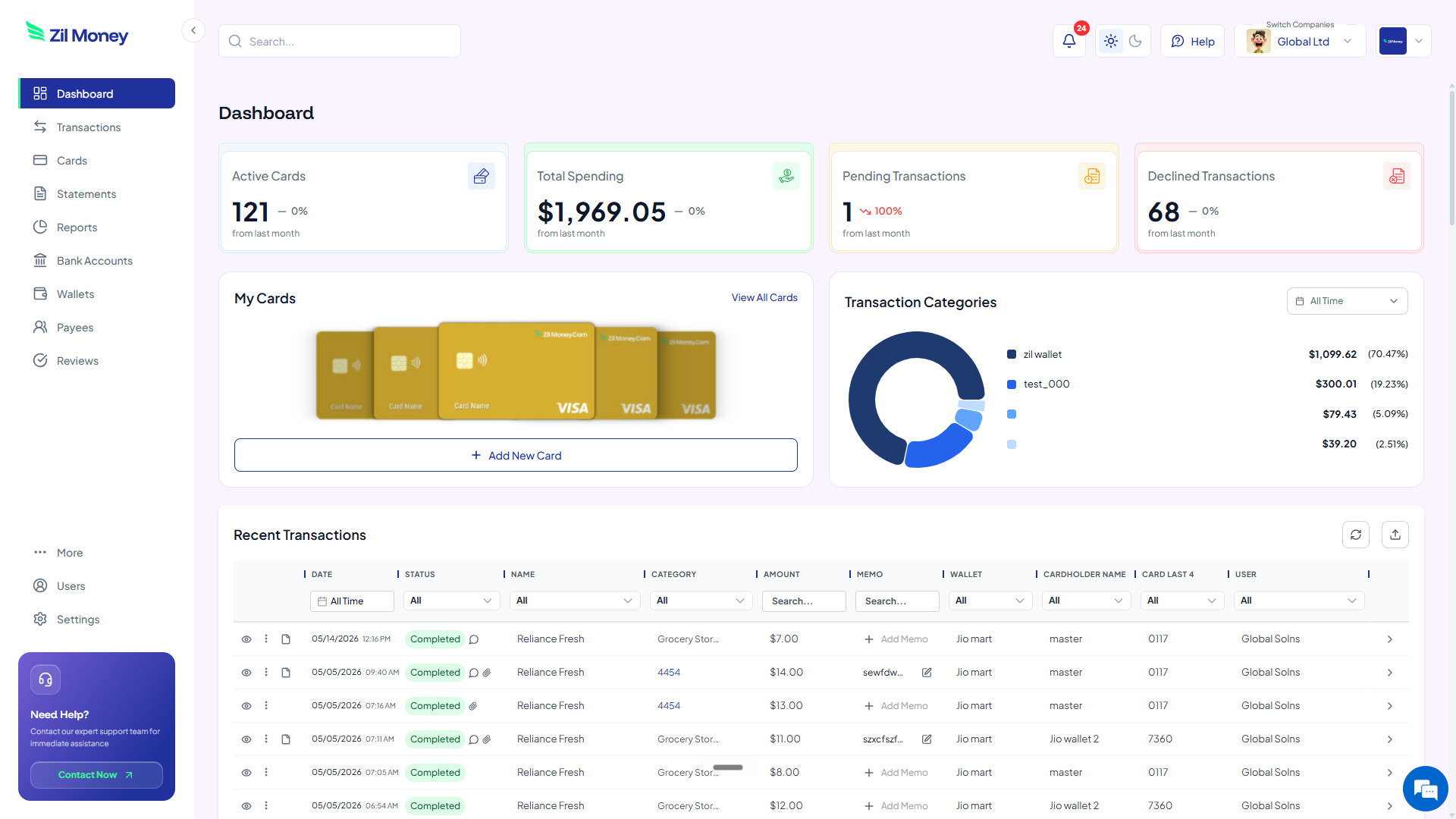

Track spend and declined attempts per card. When a campaign is winning, raise the limit on purpose. When it is wasting money, lower it. When it ends, cancel the card. You keep a per-card record of every dollar that account spent.

Running ads across several accounts?

Cap each one with its own virtual Visa and put a hard ceiling on every channel.

Ad billing with virtual cards vs one shared card

This isn't about virtual cards being clever. It's that the month-end billing surprise simply stops happening. Here's the side-by-side.

The same company card on every ad account.

- One card sits on every platform, so any single spike pulls from all of them.

- A billing glitch or runaway campaign drains the card before you can react.

- You untangle channel spend from one blended statement after the fact.

- An agency or team can overspend a budget with no hard stop in place.

- If that card is compromised or declined, every campaign pauses at once.

One card per account, capped at its budget.

- Each account has its own card, so a spike is contained to that card's limit.

- An overspend attempt above the limit can be blocked by your controls.

- Each channel's spend is already its own clean, exportable record.

- Client and team budgets are capped by the card, not by good intentions.

- If one card has an issue, the rest of your accounts keep running.

Three ad-spend moments where a virtual card saves you

Big ideas are easy to nod along to and forget. Here are three real moments when a capped card pays for itself, often in a single billing cycle.

The campaign that scaled overnight

A creative takes off, or an automated bid strategy gets aggressive, and a campaign that spent $200 a day yesterday is spending $2,000 today. On a shared card, you find out when the charge clears. On a capped card, spend above the limit can be blocked by your controls and you see the declined attempt in your dashboard. Then you decide on purpose: raise the limit to ride the winner, or hold the line.

The agency managing five client ad accounts

An agency runs paid media for five clients, each with a different monthly budget. Instead of one card and a spreadsheet of trust, the agency issues one card per client, capped at that client's media budget. No client's campaigns can ever spend another client's money, and each card is a ready-made record for the monthly invoice.

The test account nobody turned off

Someone spun up a “quick test” on a new channel three months ago and forgot it. On a shared card, it quietly spent the whole time. With a capped card per account, the test could only ever spend its small limit, and the dashboard made the stray spend obvious the first time anyone looked.

Ad spend, deductions, and clean records

Advertising is a normal, deductible business expense, but a deduction is only as good as the records behind it. When all your ad spend runs through one card, separating it by channel, campaign, or client at tax time becomes a reconstruction project. The IRS expects businesses to keep records that support what they claim, and its small-business recordkeeping guidance spells out why that documentation matters.

One card per account does the sorting for you. Each card already holds the spend for one channel or one client, so you can export it for your accounting workflow without untangling a blended statement. When a client or your accountant asks “what did we spend on this channel,” the answer is one card's history, not a weekend of detective work.

If your ad budgets are part of a wider team-by-team spend structure, the department budgets guide shows how to extend the same one-card-per-line approach across the whole company.

Why marketers prefer running ads this way

The worry marketers raise is whether a hard cap will throttle growth. In practice it does the opposite. A cap does not stop you from scaling, it stops you from scaling by accident. When a campaign earns more budget, you raise the limit deliberately, with eyes on the numbers, instead of discovering the overspend two weeks later on a statement.

It also makes experiments safe. Testing a new channel stops being a leap of faith when the most it can cost is the small limit you set. You launch more tests, kill the losers fast, and pour budget into winners on purpose, because every account has a number you chose, not a number the platform chose for you.

Set up your first ad-account card this afternoon

If you have an ad account billing to a shared card right now, here's the simplest next step.

- Sign up. Create an account at Virtual Card Maker. Getting started is straightforward.

- Add funds. Load your wallet with enough to cover this month's media budget. You do not have to prefund the whole year.

- Create the card. Set the limit to the account's monthly budget and label it by channel or client.

- Update the billing method. Swap the shared card in the ad platform for the new card, and restrict it to that platform where supported.

- Manage from the dashboard. Raise the limit when a campaign wins, lower it to slow down, and cancel the card when the account is retired.

That's the whole workflow. Start with one account, then give every channel and client its own capped card. Most teams that try it once never put all their ad spend back on a single card.